Important Notice: We are aware of fraudulent investment schemes claiming to be from Kent Reliance. Genuine Kent Reliance savings products are available only through our official channels, including this official Kent Reliance website and through our Branch Network. For further guidance on protecting yourself from fraud, please visit our

Important Notice: We are aware of fraudulent investment schemes claiming to be from Kent Reliance. Genuine Kent Reliance savings products are available only through our official channels, including this official Kent Reliance website and through our Branch Network. For further guidance on protecting yourself from fraud, please visit our

Paying Money In

You can deposit as and when you want within the first 14 days of opening your Account. You can pay money into your Account by Electronic Transfer from your Nominated Account or from another account you have with us operated using the same Online Services.

Note: For Fixed Rate Bonds, you will be unable to make any further deposits after 14 days.

Confirmation of Payee (CoP)

CoP has been introduced by the finance industry to help tackle fraud. Keeping your money safe and secure is a top priority and this new account name checking service is in place to ensure you're sending your payment to the correct person or business.

When Paying Money In by Electronic Transfer you must provide your bank with our sort code 60-84-56* and account number of your Account held with us.

Always double-check the account name and details are correct. If you would like to send a test payment of a smaller amount to see this reach your savings account first before transferring a larger amount this can be done.

*Please note our sort code is provided by NatWest as it acts on our behalf as our clearing bank.

Confirmation of Payee checks will be available from the day after your account is opened. For more information, visit our dedicated Confirmation of Payee page on our website.

You can pay money into your account, subject to the specific terms and conditions of any particular account.

The table below sets out:

- The various ways you can pay money into your account, depending on how you opened it.

- When those funds will be available to withdraw.

- If payable, when interest will be earned.

Channel by which account was opened |

|||||

|---|---|---|---|---|---|

| Branch | Post | Online | Interest | ||

| Cash | You can make cash deposits at any of our branches. The funds will be available in your account the same day. | You cannot make cash deposits into this type of account. | Where interest is payable, interest will be earned from the day the funds are deposited into your account until the day before withdrawal, closure of transfer. | ||

| Cheque | You can pay in a cheque at a branch. | You can send a cheque to our Customer Services address: OneSavings Bank, Sunderland, SR43 4AB | Where interest is payable, interest will be earned from the day the funds are deposited provided the cheque is deposited before 12pm on a working day. See section below for further information relating to when interest is earned. | ||

| Electronic Transfer | You can make electronic payments (e.g., CHAPS, bank transfers) from another account held with us or another bank/building society into your account. The funds will usually be available as cleared funds in your account on the same working day we receive them. When making an electronic payment to us, please note our sort code is provided by NatWest as it acts on our behalf as our clearing bank. | Where interest is payable, interest will be earned from the working day that we receive the funds until the day before withdrawal, closure or transfer. | |||

If you’re simply paying in money into a Kent Reliance account held by someone else in branch, we’ll record the deposit on our banking system and give you a receipt, but we won’t update that account holder’s passbook unless they’re present. Account holders shouldn’t give their passbooks to anyone else.

How we treat cheques

| Branch account | Postal and online accounts |

| Cheques deposited at a branch on a working day will, if payable, begin to earn interest the same day. Cheques deposited on a non-working day will, if payable, begin to earn interest the next working day. | Cheques received after 12.00pm on a working day or on a non-working day will, if payable, begin to earn interest the next working day. |

Cheques should be made payable in your name(s). Please write your account number and address on the reverse of the cheque.

You must allow six clear working days for clearance on all cheques paid in before a withdrawal can be made against them. We’re not responsible for the early clearing of any cheques.

Confirmation of Payee (CoP)

CoP has been introduced by the finance industry to help tackle fraud. Keeping your money safe and secure is a top priority and this new account name checking service is in place to ensure you're sending your payment to the correct person or business.

Please be aware that Confirmation of Payee checks will not be available until the day after your account is opened. If you choose to fund your savings account on the same day it is opened, Confirmation of Payee validation will not be available. You may not be able to deposit funds into your account straight away, depending on the bank/building society you have your Nominated Account with. If you receive an error message, please wait until the next day to deposit funds into your account. This will allow for the CoP checks to clear.

When you're setting up an electronic payment from your external bank account to a Kent Reliance account you haven't paid into before, be sure to use the payee information exactly as detailed below.

Electronic payments and standing orders

To fund your account by electronic payment or standing order (subject to the specific terms and conditions of your account), you’ll need to quote the following details:

| Payee Name | This will be the name of the Account Holder for the account you are funding |

| Sort Code | 62-24-97 * |

| Account number | 01234567 (take the numbers from your account number and add a ‘0’, as shown in the example) (example e.g., ABC1234567KRB would become 01234567) |

| Reference | ABC1234567KRB (quote the full account number of the account you’re paying into, including the letters at the beginning and the end, as shown in the example) |

| Account type | Select ‘Personal’ or ‘Business’ depending on Payee Account type |

Funds will usually be available as cleared funds in your account on the same working day we receive them.

Please note: the above details cannot be used for CHAPS payments

CHAPS

To pay money in by CHAPS (payments will be processed the same working day if they’re received by 4pm) please use the following details:

| Payee Name | This will be the name of the Account Holder for the account you are funding |

| Sort Code | 60-05-09 * |

| Account number | 55258085 |

| Reference | ABC1234567KRB (quote the full account number of the account you’re paying into, including the letters at the beginning and the end, as shown in the example) |

| Account type | Select ‘Personal’ or ‘Business’ depending on Payee Account type |

Please note: that your bank/building society may charge for sending funds to us via CHAPS

Funds will usually be available as cleared funds in your account on the same working day we receive them.

*Please note our sort code is provided by NatWest as it acts on our behalf as our clearing bank.

Please note: Confirmation of Payee checks will be available from the day after your account is opened. For more information, visit our dedicated Confirmation of Payee page on our website.

Taking Money Out

You can only make payments out of your account into your Nominated Account (or another account you have with us if your Specific Conditions allow) by Electronic Transfer. To make a withdrawal you can simply log in to our Online Services.

You can only make payments out of your account if you have enough money in your account to cover the payment. Please check the Specific Conditions of your Account to ensure withdrawals are permitted.

For Fixed Rate Bonds, you can cancel your account within 14 days of opening it by logging into our Online Services. No further withdrawals are permitted during the fixed rate period.

We understand that things can change unexpectedly and so, if you have an account that doesn’t allow access and you require your savings earlier or before your maturity date, you can call us to discuss this. We may ask you to help us understand your change in circumstance which may include a request for supporting documents. Any decision that is made, is at our discretion.

We may apply financial and other limits to Electronic Transfers from your Account. You cannot request withdrawals totalling more than £30,000 on a Saturday, Sunday or English public holiday as this goes over the limit we have in place. As our withdrawal limit refreshes daily, you can request your amount over multiple days. Please note, you will only be able to withdraw up to £30,000 across all account(s) you have with us.

There are no limits for transferring funds to another account you have with us e.g. you can make a payment for any amount at any time and the payment will reach your account the same day.

Please see the table below for further information on our withdrawal limits and when your payment will likely reach the bank where your Nominated Account is held:

| Withdrawal amount per day | When we treat your payment instruction as received | When your payment will usually reach the bank where your Nominated Account is held | Example |

|---|---|---|---|

|

£0 to £30,000 |

The day you give us the instruction. |

The day you give us the instruction. |

You ask us to make a payment on Monday. It will usually reach the bank where your Nominated Account is held on Monday. |

|

Over £30,000 |

The Working Day you give us the instruction. |

By the end of the next Working Day. |

You ask us to make a payment on Monday. It will usually reach the bank where your Nominated Account is held by the end of Tuesday. |

|

Working Days are any day other than a Saturday, Sunday or an English public holiday. |

|||

If you wish to close your Account on a non-Working Day and your total withdrawal request exceeds £30,000, you must submit your request on the next Working Day. Please note, you can still withdraw up to £30,000 on a non-Working Day.

You can withdraw online, by post and in branch, depending on your account terms. Electronic payments from your account can only be credited to your nominated bank account.

How to request a closure?

You can close your account by phone or by post. If you have registered for Online Services then you can also send us a secure message. If you have a branch-based account then you can you visit one of our branches. If you close your last active account, you’ll no longer be able to access online services. If you send us a secure message to request closure, you will not be able to view a response. We recommend that before closing, you download any information or statements you would like to keep on record.

How to make a withdrawal? Online and Postal accounts

You can make a request to withdraw money online (if you have registered for Online Services), by phone or by post. If you have a branch-based account, you can also visit one of our branches.

For notice accounts

Not all notice accounts allow withdrawals without giving the full amount of notice. If your account allows immediate access, it will be subject to a loss of interest.

Please refer to the product specific terms and conditions of your account for further details.

For fixed term accounts

If your bond allows you to make a withdrawal during the fixed rate period, it will be subject to a loss of interest.

Please refer to the product specific terms and conditions of your account for further details.

We understand that things can change unexpectedly and so, if you have an account that doesn’t allow access and you require your savings earlier than your notice period allows or before your maturity date, you can call us to discuss this. We may ask you to help us understand your change in circumstance which may include a request for supporting documents. Any decision that is made, is at our discretion.

What will I need to make a withdrawal or closure?

By post

A signed letter detailing your request or alternatively, you can download and complete a withdrawal/closure form. Please send your request to OneSavings Bank, Sunderland, SR43 4AB.

Online/by phone

- The date you want your money to leave your account, or when you would like your account to close; and

- The amount you would like to withdraw, and/or confirmation that you would like to close your account (if applicable).

In branch

Please bring your passbook (if applicable) and identification with you. You can find a list of the documents we accept in our Proof of ID and address leaflet.

For details on how to get in touch, visit our contact us page.

Electronic payment requests

Electronic payments (e.g. CHAPS, bank transfers) will only be sent to your nominated bank account. If you change or add a new nominated bank account, please allow additional time for the change to take effect. It’ll take one working day to validate your new nominated bank account, which will result in the payment timescales being delayed by one day. Click here for further information about nominated bank accounts.

If we receive your payment request before 3.30pm on a working day your money will be transferred to the receiving bank/building society on the same day you requested them.

If we receive your payment request after 3.30pm or on a non-working day (weekends and bank holidays), your money will be transferred to the receiving bank/building society the next working day.

Please note CHAPS requests cannot be made online. Please call us if you want to make a CHAPS payment, these may incur a charge.

Please be aware that if you send us a withdrawal/closure request by post, you may receive your money a day later than the timescales shown above.

There is no limit on how much you can withdraw, subject to money being available in the account and your specific terms and conditions.

Cash withdrawal requests

Cash withdrawals can only be made by customers who opened their account(s) in a branch.

Cash (requested at branch during branch opening hours) |

|

|---|---|

| How much can I withdraw? | When will I receive my money? |

| Our current daily cash limit is £500 | Same day (over the counter) |

| Withdrawals in excess of £500 must be paid by cheque or electronic payment. (e.g. CHAPS, bank transfers) | |

Cheque withdrawal requests

Cheque withdrawals aren’t available for accounts opened online.

Cheques |

||

|---|---|---|

| Method of request | How much can I withdraw? | When will I receive my money? |

| Branch (requested during branch opening hours) |

Up to £99,999.99 | Same day (over the counter) |

| £100,000 and above | Your cheque will be processed at our Customer Services office and posted to your registered address. Please see tables 4 and 5 of the Savings General terms and conditions for further details. |

|

| Post/telephone |

No limit, subject to money being available in the account | Your cheque will be posted to your registered address the day your request is treated as received. Please see tables 4 and 5 of the Savings General terms and conditions for further details. |

Nominated Bank Accounts

What is a Nominated Bank Account?

A Nominated Bank Account is a current account with another UK bank/building society held in your name that has been registered and verified by us. Your Nominated Bank Account is where all electronic payments (apart from internal transfers) out of your Kent Reliance account must be sent to.

Does the Nominated Bank Account have to be solely in my name or can it be a joint account?

Your Nominated Bank Account can be a sole or joint account. Any current account that you’re named on can be used as a Nominated Bank Account.

Do I have to have a Nominated Bank Account?

In order to send an electronic payment in or out of your Kent Reliance account, we require a Nominated Bank Account to be registered and verified by us before the payment request is received.

Can I change my Nominated Bank Account?

Yes, you can change your Nominated Bank Account. The process depends on your account type:

- For accounts starting with letters (e.g., ABC123456SNA):

- Visit one of our branches for assistance.

- Or, call us or send a letter along with a valid bank statement. You can find our contact details on the Contact Us page.

Important:- If you are making a withdrawal and changing your Nominated Bank Account at the same time, electronic validation of the new account will take one working day to process. If you are only changing your Nominated Bank Account, the update may take up to 5 working days.

- If electronic validation isn’t possible, we may ask for an original bank or building society statement (no older than three months) showing your account details. Until the change is complete, any withdrawals will continue to be paid into your existing Nominated Bank Account.

- For accounts starting with numbers (e.g., 12345678):

- You can change your Nominated Bank Account easily online by logging into your account.

How do I set up a Nominated Bank Account?

For accounts starting with numbers (e.g 12345678), you would have set up your Nominated Bank Account during the application process.

For accounts starting with letters (e.g ABC123456SNA), you must provide details of a valid UK bank/building society current account for your Nominated Bank Account. We’ll electronically verify that this account is held in your name (or in the name of the first applicant for a new joint account application). If we cannot verify this information electronically, you may be asked to provide additional evidence, e.g. an account statement.

Can I have multiple nominated bank accounts?

No. Each customer may only have one Nominated Bank Account. This will be used for withdrawals/payments on all accounts held with us.

We have a joint account, can each of us have our own Nominated Bank Account?

Yes. When opening a joint account, the first applicant must be named on the Nominated Bank Account for identity verification purposes. Once set up, additional account holders can have a different Nominated Bank Account associated with the joint account.

Register for Online Services

If your account number has a combination of letters and numbers, for example ABC1234567SNA, please visit register for Online Services for further information.

Changing your account details

It’s important that you let us know of changes to important information such as your name, address, telephone number or email address. You can let us know about any changes in the following ways:

If you have an account that is operated by our branch team, then you can simply pop into your local branch. Please bring your passbook, another form of identification and evidence to confirm the changes.

If you have an account number that starts with numbers (e.g 12345678) then you can change any of your personal details by logging into your account, please ensure you have your login details and mobile phone to hand to do this.

If you have an account number that starts with letters (e.g ABC1234567SMI) then you can log in to Online Services and send us a secure message. We’ll aim to first verify the changes electronically, but may require you to provide evidence to confirm the changes if we’re unable to verify them online.

You can also call our Customer Services Team. We’ll need to ask you some questions to verify your identity and may require you to write or provide evidence to confirm the changes.

Writing to us at OneSavings Bank, Sunderland, SR43 4AB. Please make sure you sign your letter and provide evidence to confirm the changes.

Moving Abroad

How does my move abroad affect my account?

You must tell us of this change in circumstance straight away so that we can help you manage your account.

If you have an easy access or notice account, we won’t be able to accept any further deposits into it and you won’t be able to open any new accounts with us.

If you have a fixed rate account you’ll be able to open another account offered by us when your account is due to mature from the maturity options available and then transfer your savings to that account upon maturity. However, you will not be able to add any additional funds to that account or open any new accounts with us that you see on our website or in our branches.

You can review our Savings General Terms and Conditions.

We are continuing to monitor any impact of the UK’s withdrawal from the EU and are here to support you if you are affected by any changes.

If you plan to move to any of the following countries, you will no longer be eligible to save with us and the account(s) will need to be closed:

- Netherlands

Please contact us, if the above applies to you. We want to make this process as easy as possible so please be assured we’re here to help.

If we do need to make any changes to our products or the way we service any of our non-UK resident customers, we’ll be sure to contact you and give you as much notice as possible.

Fees and Charges

| Fee or Charge | Amount |

|---|---|

| Replacement passbook The first replacement passbook is free - any subsquent replacements are £10. |

£10 |

If we increase or add a charge, we’ll notify you personally at least 30 days before the charge comes into effect.

Lost and Forgotten Accounts

If you think you may have lost or forgotten about a Kent Reliance account, here is some information about what you should do and how we will do our best to help you.

If you think you’ve lost track of or forgotten an account with us, we’ll help you to trace your money.

Where there has been no customer initiated transactions (e.g. withdrawal, deposit or maturity instruction (if applicable) on your account for a continuous period of 6 years or more, we may mark your account as inactive.. We may at our discretion mark an account as ‘Gone Away’ if on more than two occasions items of post are returned to us.

We stop sending letters and statements to inactive accounts, to avoid the risk of personal information being sent to the wrong address.

If an account of yours has been marked as inactive we will need to confirm your identity (ID). This is to prevent fraud and to protect your money.

In the case where the account holder has died, we’ll have to confirm both the ID of the person claiming the funds, and that they have a legal right to the funds – for example, they may be an executor of the estate.

When the ID checks have been carried out successfully, the account funds can be released, together with accrued interest. In all cases, the funds in the account remain the property of the account holder or, in the case of death, their estate.

If you think you have any account with us that may have been flagged dormant, inactive or ‘gone away’, please complete our Form to Reclaim Lost Funds to begin the process of recovering the funds. Once completed, you can return the form to us by post at the address below:

OneSavings Bank

Sunderland

SR43 4AB

Coming to the end of your Fixed Rate Bond

Prior to maturity, we'll contact you and outline all your available options. Please refer to the information provided in your maturity choices pack to guide you through this process.

To open a new Fixed Rate Bond or Easy Access Savings Account online through our website:

- Choose to close your maturing bond. We'll initiate the return of your money to your Nominated Account on the maturity date. You can let us know by filling out the details on page C of your maturity choices pack, calling us or sending us a secure message online. Please allow up to 5 working days for your funds to be available.

- Go to www.kentreliance.co.uk/products/all-products to start the application process for a new Fixed Rate Bond or Easy Access Savings Account.

- You'll need to provide or reconfirm some of the personal details we already hold for you, including your mobile number, email address and Nominated Account details. You'll also need to set up a new username and password.

- Once you've opened your new account, you can easily transfer money from your Nominated Account straight into your new account. You'll also be able to see details of how to do this in your welcome email and when you log into your new account.

Important: If you are the operator of an account holder who is under the age of 18, you won't be able to apply online for a new account. Contact us so we can support you through your options.

About our new Online Services

Easily access answers and solutions to all your account and login-related concerns here.

Bereavement

If you’ve lost someone, it may be a struggle to know what steps you need to take next. We’ve provided information below to help you through this difficult time. If you have any additional questions about our bereavement process, or if you need support, please get in touch.

Please note this information is for savings customers only. If you’re a mortgage customer, please click here.

With you every step of the way

There can be a lot to think about when you lose someone close to you. That’s why we’ve put together an overview of the important things you need to consider during this difficult time.

Step 1

Register the death

It's a legal requirement to do this within five days of the death.

Step 2

Arrange the funeral

Contact a funeral director to begin making arrangements.

Step 3

Is there a will?

Check to see if one exists.

Step 4

Who to contact

Inform any financial or legal bodies as early as possible.

Step 5

Manage the estate

If there is a will, this will help you deal with the estate’s distribution.

Step 6

Seeking further help

Reach out to others if you need emotional support.

Step 1

Registering a death

Every death must be registered at the local registry office. This must be done within five days (eight days in Scotland), unless it has been referred to the coroner.

This is a legal requirement and the registrar provides a formal record of death (a death certificate).

What do I need to be able to register the death?

You’ll need to take the following documents/information with you when registering the death.

Personal information about the deceased (please see the checklist in the ‘Who to contact’ section to assist with this).

Medical certificate – this certificate is free and should be provided by a GP or doctor; or

Coroner’s certificate – in certain circumstances a death has to be investigated by the coroner.

The registrar won’t charge for issuing the death certificate. You may want to think about buying extra official copies of the death certificate, as this can be helpful when dealing with the deceased’s estate.

Step 2

Arranging the funeral

Contact a funeral director to begin making arrangements. Most funerals are arranged and take place within a week or two following death. It’s important to say goodbye. Funerals can be expensive, so it’s worth checking to see if a prepaid funeral plan or life insurance policies exist that may help to cover the cost. If there are sufficient funds in the deceased’s Kent Reliance account(s), these can be used to cover the funeral costs without having to wait for the Grant of Probate to be issued. These funds will be sent directly to the funeral directors.

Step 3

Is there a will?

If there’s a will, it may be held with a solicitor, or at the deceased’s home. A will explains what should happen to the deceased’s estate. It’s their last wishes as to what happens with their assets and funeral arrangements. If there’s a will, it names the executor(s) chosen by the deceased to deal with their estate.

If there isn’t a will

Where the deceased has not left a will, their estate will be dealt with under the laws of intestacy. These laws set out who should deal with and benefit from the estate; this will usually be the next of kin. In some cases, “Letters of Administration”, issued by the Probate Registry will need to be applied for. This document authorises the appointed administrator to deal with the deceased’s estate. We suggest you contact your local Citizens Advice Bureau or solicitor if you require further support with this.

A Grant of Probate or Letters of Administration can also be called a ‘Grant of Representation’.

Throughout this page we’ve assumed that if one is required, the deceased representative will apply for a Grant of Probate. However, there may be cases where Letters of Administration will need to be applied for.

Step 4

Who to contact

When you register the death, the registrar will direct you to the government service ‘Tell Us Once’, which can be found at gov.uk/after-a-death/organisations-you-need-to-contact-and-tell-us-once; this enables you to contact various government departments in one go. This service is offered by most local authorities in England, Wales and Scotland, except Northern Ireland.

If the service isn’t offered by your local authority, then you may need to notify the following:

- HM Revenue and Customs (HMRC)

- The Department for Work and Pensions (DWP)

- HM Passport Office (HMPO)

- Driver and Vehicle Licensing Agency (DVLA)

- Local council

You may also have to inform other organisations. These could be legal, financial and social organisations that need to be informed as soon as possible.

Organisations you may need to contact:

- Banking and Building society providers

- Mortgage provider, landlord or local authority

- Royal Mail (for post redirection)

- Utility companies (water, gas, electric and phone)

- TV licensing and broadband companies

- Any clubs

- Dentists, doctors, hospitals or opticians

- Local church or regular place of worship

- Charities and/or care homes

To make sure that there are as few complications as possible in the notification process, it’s important to gather as much of the following information as you can about the person who has died.

We’ve created a checklist to simplify matters for you: Download checklist

Step 5

Manage the estate

The first step to valuing the estate is to identify the assets and liabilities of the deceased. Liabilities could include personal loans, credit cards, hire purchase agreements, outstanding tax, etc. Assets could include property (less any mortgage), value of personal belongings, shares and monies that are held with other banks or building societies. Any assets will need to be valued in order to distribute the deceased’s estate and if appropriate, to obtain a Grant of Probate.

Grant of Probate

A Grant of Probate is an official legal document which gives the authority to the deceased’s executors to act on behalf of the deceased when dealing with their estate. In Scotland, this is known as Grant of Confirmation.

Steps to take when applying for Grant of Probate

Once you’ve assessed the value of the estate and paid any required inheritance tax, the Grant of Probate will be issued. To apply for a Grant of Probate, a probate application form (PA1) must be completed. This can be downloaded from the HM Courts and Tribunals Service website at gov.uk. The completed application form can be submitted by post or via the government’s website. You can either choose to do this yourself or you can obtain the help of a solicitor.

Informing Kent Reliance when a customer dies

When it comes to informing us of the death of a customer, we want to provide as straightforward a process as possible. You can let us know as soon as possible of the death by contacting us on 0345 122 1120.

What we’ll need from you

In order to close an account, our Customer Services Team will ask you to download and fill in the below form, scan it and send it to us via email customerservice@kentreliance.co.uk. This form will highlight any additional information/documentation we may need in order to assist you through this process.

Informing Kent Reliance when a customer dies

When it comes to informing us of the death of a customer, we want to provide as straightforward a process as possible. You can let us know as soon as possible of the death in a number of ways:

Visit your local branch:

(See our branches for your nearest locations)

Call us on:

0345 122 1122

Write to us at:

OneSavings Bank, Sunderland, SR43 4AB

Once we've been notified, we can let you know what the next steps are and we'll take the appropriate action to safeguard the funds.

What we’ll need from you

The first thing you’ll need to do is provide us with the original, an official or certified copy of the death certificate or coroner’s certificate. These will be returned to you. Please note, whilst the original death certificate can be taken into your local branch, we don’t advise you send these in the post. We recommend you send through the post either an official copy or a copy certified by a solicitor.

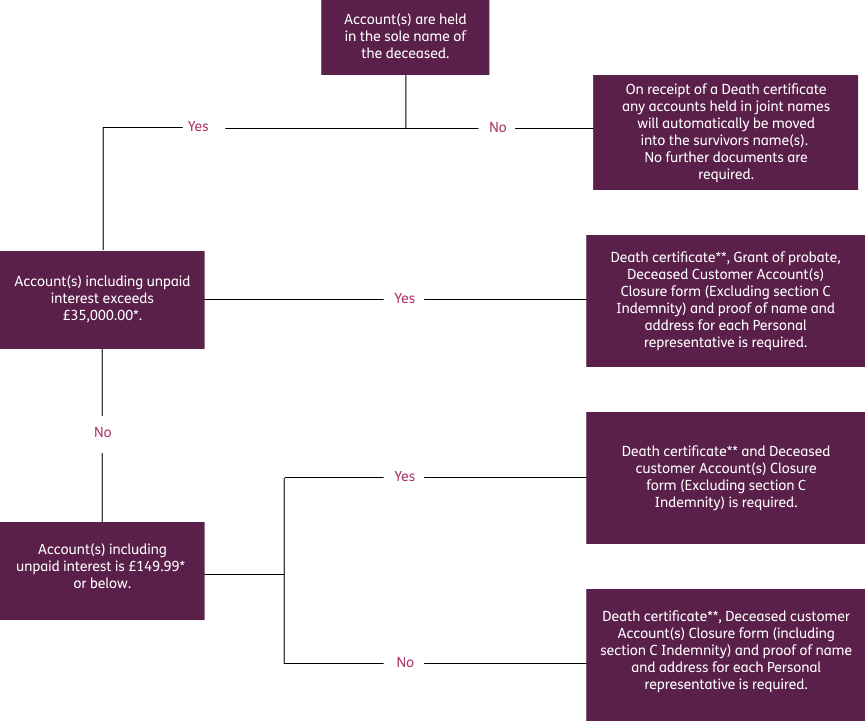

Once you’ve completed the form and we’ve received evidence of the death we’ll be able to update our records. If you hold accounts on both of our Online Services systems, we will ensure the records are updated on both. From this point, we won’t send any further correspondence to the deceased customer. We won’t be able to accept any further deposits into the deceased’s Kent Reliance account(s) (If any payments are received after the death has been registered with us, we'll return the funds to the originating account). If the account is held in joint names, we can continue to accept deposits on behalf of the remaining account holder. If you do write to us, please include your address and contact number.

Please note

-

If the deceased funds are held in a fixed term bond, ISA or notice account, there will be no loss if interest applied to the closure of account.

-

Interest will continue to accrue until the account is closed

-

The account will stay open until we receive appropriate documentation to close it

-

For joint accounts, ownership will transfer to the other account holder(s)

-

If the deceased held an ISA with us the surviving spouse/civil partner may be eligible to take part in the Additional Permitted Subscription (APS) ISA scheme. Kent Reliance do not currently offer APS ISA accounts however you are able to transfer the allowance to another provider if they accept them.

The next steps will depend on the total balances held with us.

What we need if there’s a Grant of Probate

Once probate has been granted, we’ll need to see either the original, official copy or certified copy of the Grant of Probate and be provided with a completed Deceased customer account(s) closure form. In normal circumstances, these documents can be provided to us by sending them through the post or by visiting your local branch. We’ll then take copies and return the documentation to you. We recommend you do not send the original Grant of Probate through the post.

Documents we will need from you to close the deceased customer’s account(s)

*Please note, if the total balance of the deceased’s account(s) was £35,000.00 or above as at the date of death but has since fallen below, we will still require a grant of probate/letters of administration to close the account.

**If we have previously had sight of the death certificate, we will not need to see it again when closing the account.

Once all of the required documents have been received and payments made following the instructions on the Deceased customer account(s) closure form we’ll close the deceased’s account. Please see below for further details.

Please note

We can only release funds to the Personal Representative(s) or solicitor dealing with the estate as mentioned on the Deceased customer account(s) closure form.

Certain validation checks may need to be made by us if the funds are to be transferred to another bank or building society.

We’ll require a recent bank statement to confirm the bank account details mentioned on the Deceased customer account(s) closure form.

We’ll require a recent bank statement or voided cheque to confirm the bank account details mentioned on the Deceased customer account(s) closure form. Alternatively, a cheque can be made payable to the Personal Representative(s) or solicitor and sent to the address provided on the Deceased customer account(s) closure form.

For balances up to £149.99

If the account balance is below £149.99 (including unpaid pending interest), it can be closed by providing the death certificate and the completed Deceased customer account(s) closure form.

Exceptions

We can make certain payments from the deceased account before we receive the Grant of Probate (if appropriate) or the completed Deceased customer account(s) closure form. These are:

-

Funeral costs - once we have been provided with the funeral directors’ original invoice, arrange payment directly to the funeral director to cover these costs.

-

Inheritance Tax - once we have been provided with a completed IHT423 form, we’ll arrange for a bank transfer to be made to HMRC for the amount of tax due. Once completed, we’ll send confirmation of the payment to the person dealing with the estate. Please submit a separate form for each account. An IHT423 can be downloaded from the HMRC website.

Step 6

Seeking further help

Below is a list of other organisations you can contact that provide specialist financial and emotional support to people who’ve been bereaved.

|

|

|

|

Citizens Advice |

Cruse Bereavement Care |

|

Free help and advice concerning financial and legal matters. |

Support and guidance for people that have lost someone. |

|

|

|

|

Child Bereavement UK |

Mind |

|

Helps young children and young people (up to age 25), parents, and families, to rebuild their lives when a child grieves or when a child dies. |

Mental health charity that offers support and personal wellbeing advice. |

|

|

|

|

CALM |

|

|

The Campaign Against Living Miserably (CALM) is leading a movement against suicide through frontline services, national campaigns and by building communities. Their helpline and webchat is open 365 days a year from 5pm - midnight. |

|

We’re here to help

We hope that this has provided you with the essential information you may need. However, if you’d like someone to walk you through the steps you need to take in person, please let us know and we’ll do what we can to help. If you still have some questions or would like clarification on any of the information provided, please don’t hesitate to get in touch.

How to Complain

At Kent Reliance we’re committed to giving you the best service at all times. However, if we don’t deliver the standard of service you expect, or if we make a mistake, we need to know so we can put things right. So if you’re unhappy with any aspect of our service, please tell us. We will investigate the situation and set about putting it right as quickly as we can.

To make it as easy as possible for you, you can find the information on this page on a PDF called How we'll put things right:

-

For Savings customers click here to view the PDF

How to make a complaint

You can telephone, write or send an email (please include your account number and a daytime contact number) detailing your complaint to our Head Office.

Opening times

Monday - Thursday 8am - 7pm

Friday 8am - 6pm

Closed weekends and Bank Holidays

* Please only use email to request a call back. As email isn't a secure channel, please don't include any sensitive or financial information in addition to your account number and telephone number in any messages you send.

What happens next?

We aim to resolve all complaints by the close of three working days after the date the complaint is received. If this isn’t possible, we’ll send you a written acknowledgement confirming your complaint has been received, together with full details of the person who is handling it.

In exceptional cases we may require up to eight weeks, or 35 working days for some complaints about electronic payments, to fully investigate your complaint and issue you with our final response.

If you’re still not satisfied or if eight weeks have passed since you first raised your complaint with us, you have the right to refer your complaint to the Financial Ombudsman Service (FOS). We’ll send you instructions of how to do so at that point.

We subscribe to the Financial Ombudsman Service

The Financial Ombudsman Service (FOS) provides consumers with a free independent service for resolving disputes with financial organisations.

The FOS will only investigate a case when the financial institution has had the opportunity to put things right. They allow Kent Reliance up to eight weeks to deal with your complaint. If you are still not satisfied, you must take your complaint to FOS no later than six months from the date of our final response letter.

Visit the FOS website for more information on complaint eligibility and how to take a complaint to them. Their address is:

The Financial Ombudsman Service

Exchange Tower

London E14 9SR

T: 0800 023 4567

E: complaint.info@financial-ombudsman.org.uk

Power of Attorney

Planning for the future

While none of us want to think about a time when we might need support to manage our affairs, having a power of attorney in place can make things much easier if that time comes.

This guide explains how you go about appointing someone to make decisions on your behalf, the different types of power of attorney, and how to register one to help you manage your account.

What is a power of attorney?

A power of attorney is a legal document that lets you select one or more trusted people to help you make decisions or to make decisions on your behalf.

There are a number of different types of power of attorney, so we recommend you seek advice on whether obtaining a power of attorney is the right option for you and, if so, which type would be best suited to your particular circumstances.

Please note, a power of attorney can be created with or without a solicitor. Even if you don't use a solicitor there will be a fee to register the power of attorney.

Why would you need to appoint an attorney?

There could be a number of reasons why you might need help managing your account or other financial affairs. You may want to ensure bills are paid whilst you are in hospital, or you may want to ensure your finances are looked after if you’ve been diagnosed with a long-term illness or disability.

Types of power of attorney

Lasting Power of Attorney (LPA) - There are two different LPAs: one for financial matters and one for health and care decisions. The LPA for financial and property decisions is the one we'll need to allow an attorney to help you manage your savings accounts with us. A financial LPA can be used by an attorney as soon as it’s registered as long as you give permission for this in the instructions of the LPA. If you want, you can also state the LPA is only to be used if you lose mental capacity. You can find out more about registering an LPA at www.gov.uk/government/organisations/office-of-the-public-guardian.

Enduring Power of Attorney (EPA) – this is an old form of power of attorney used for financial decisions. If you created one before October 2007, it’s still valid – but you can’t create a new one. For any new applications, you’d need to use an LPA.

Ordinary Power of Attorney (OPA) - For extra support during temporary situations, for example when travelling or during a planned hospital stay, there’s also an OPA. This is used for financial decisions and is only valid while both parties still have mental capacity, so it’s not an alternative to an LPA.

Who can be my attorney?

An attorney takes on a serious responsibility for making decisions for someone else. The person you choose to appoint as your attorney should be someone you completely trust. They must be over the age of 18 and have the mental capacity to make their own decisions. This could be a partner, relative, a friend or a professional e.g. a solicitor. Depending on whether you need to appoint an attorney on a temporary or long-term basis, there are a number of factors you should consider, such as:

- How well they look after their own financial affairs;

- How well you know them;

- If you trust them to make decisions in your best interests; and

- How happy they’ll be to make decisions for you.

Registering your power of attorney

If you want to add a third party (including an attorney) to help manage your account, we’ll need you to fill out our adding an authorised third party form and provide the following legal documents:

Please be aware that by registering a third party operator to support managing your accounts, you will continue to have access to our Online Services but the third party acting as an operator will not have online access.

Also note that whilst we’re in the process of building our new online services system and gradually adding new functionality, for the time being you will need to call us after each additional account you take out to add a 3rd party authority to it.

Power of Attorney document

- Certified copy of the power of attorney (we’ll require a power of attorney which specifically deals with financial and property affairs); Or

- If you have lasting power of attorney already set up and it was registered on or after 1 January 2016, you can provide us with an LPA access code. (Access codes are 13 characters long and start with a V).

Identification documents

- Personal identification for the attorney(s) being added to your account (proof of name and address); and

- Account details (If known)

You can contact our Customer Services Team to request the form and talk to us about the best way to return your documents. See details of how to contact us and when we’re available.

Registering your power of attorney

Please be aware that by registering an operator to support managing your accounts, online access will no longer be available to any account holders named or any operator(s) who have been registered.

To allow us to validate your power of attorney, you or your attorney will need to provide the documentation detailed below. You can do this by visiting one of our Kent Reliance Branches or send the documentation to One Savings Bank, Sunderland, SR43 4AB. We will return any original or certified copies to you.

Power of Attorney document

- The original or certified copy of the power of attorney (we’ll require a power of attorney which specifically deals with financial and property affairs); Or

- If have an LPA and it was registered on or after 1 January 2016, you can provide us with an LPA access code. (Access codes are 13 characters long and start with a V).

Identification documents

- Personal identification for the attorney(s) being added to your account (proof of name and address); and

- Account details (If known) (for branch-based accounts please provide your passbook).

Does marriage or civil partnership mean I’ve automatically got a power of attorney in place?

If you’re married or in a civil partnership, you may have assumed that your spouse or partner would automatically be able to deal with your bank account and pensions if you lose the ability to do so. This is not the case. Without a valid power of attorney, they won’t automatically have authority or access.

If there comes a time when you can't make your own decisions and there isn't an LPA in place, this may involve the Court of Protection. This can be a timely and costly process.

Find out more at www.gov.uk/courts-tribunals/court-of-protection

Further information

For further advice and information, contact a solicitor, your local Citizens Advice Bureau or the Office of the Public Guardian. We’ve listed some useful contact details below:

MAKE, REGISTER OR END A POWER OF ATTORNEY

Report safeguarding concerns

OFFICE OF THE PUBLIC GUARDIAN (ENGLAND AND WALES)

0115 934 2777, Text phone: 0115 934 2778

Lines are open Monday to Friday, 9.30am to 5pm

Wednesday, 10am to 5pm

Help finding a solicitor

THE LAW SOCIETY (ENGLAND AND WALES)

Additional support organisations

AGE UK

ALZHEIMER’S SOCIETY

SOLICITORS FOR THE ELDERLY

Additional support

We recognise that certain customers are at greater risk of poor outcomes when dealing with their finances and vulnerability can arise for a wide range of reasons.

No matter what support you need, or situation you’re facing, we’re here to help in any way we can. We know there’s no one-size-fits-all approach, so we’ll take the time to understand your needs and respond with sensitivity, respect and compassion.

Here are just some of the ways we’re committed to supporting our customers:

- We promise to remain open and approachable, and to listen and respond to our customers with sensitivity and respect

- We’ll treat every customer as an individual and do everything we can to understand and support their needs

- Our policies, products and services will be regularly reviewed and updated, to help improve the overall customer experience

- Our colleagues will be provided with the skills and training they need to support all customers

- Our communications will remain clear, accessible and easy to understand

- If further help is needed, we’ll signpost to other relevant organisations, such as charities and advice services

Ways we can help

How we have set up our Kent branches:

- All branches have a power-assisted or automated entrance door.

- All branches are level access or have wheelchair ramps

- We welcome all assistance dogs

- We provide seating areas

- All branches have a low level counter or separate desk

- Private office spaces

- Induction loop (At least one counter with an induction loop as well as a portable induction loop to use in other areas of the branch.)

- We have removed the dark flooring from some of our branches

- In some branches we support the use of toilet passes.

Equipment available in our branches:

If you find it hard to use your hands, sign your name or read information, these are some things that may help. Just ask one of our branch team:

- magnifiers

- Weighted pens

- Signature guides

- Reading glasses

- clipboards

- Coloured acetate sheets. Some colours are held in branch and others can be ordered

- Yellow printing paper

- Portable chairs

All our branches offer appointments subject to availability. To book an appointment in one of our private meeting rooms you can call our customer service team and request for a member of your nearest branch to call you and arrange an appointment.

Don’t see a support that helps your situation? let us know in person or over the phone to discuss alternative arrangements.

To find you nearest branch click here to use our branch finder.

Power of attorney

To find out what steps you need to take to register a Power of Attorney to an account, please go to our power of attorney page.

Bereavement help and support

There can be a lot to think about when you lose someone close to you. That’s why we’ve put together an overview of important things you need to consider during this difficult time.

Protecting yourself against fraud and scams

In our guide to fraud and scams you can learn how to spot a scam and keep your money safe, as well as know the risks, look out for the tell-tale signs, and have peace of mind when managing your finances.

Support with financial difficulty

We understand the worry and concern you may face if you’re having difficulties in meeting your mortgage repayments. Our financial difficulties support page explains what we can do to assist you and steps you can take to help yourself.

Third party authority

If you need to appoint a third party to discuss your account with us, please get in touch.

External resources

Financial abuse

If you’ve been a victim of financial abuse, UK Finance’s “It’s your money” guide provides information on what support is available to you.

Further support and advice

We’ve compiled a list of organisations who have the expertise, skills and knowledge and provide the support or advice you might need.

Power of attorney

To find out more information about a power of attorney, please visit https://www.gov.uk/power-of-attorney

How to contact us

If you have any questions or concerns about any aspect of managing your account, or want to speak to someone about any extra support you need, there are a variety of ways you can contact us:

- To speak to someone in confidence, please get in touch

- Write to us at OneSavings Bank, Sunderland, SR43 4AB

- Email us - Please only use email for general enquiries or to request a call back. As email isn't a secure channel, please don't include any sensitive or financial information in any messages you send. Please visit our Protecting yourself against fraud and scams page for more information.

- Alternatively, if you’re an existing customer with an online account, you can contact us using secure message.

- For savings customers, you can visit us in one of our branches.

The details you provide to us will be used sensitively to help us support you with managing your account and in line with our Privacy Notice, which you can view at https://www.kentreliance.co.uk/legal/privacy-policy. We’ll be happy to answer any questions you have about how we process your personal information when you contact us.

Using our website

Improving our website accessibility is an ongoing priority for us, to ensure we keep up to date with website standards and enhancements in technology. Please tell us if you’re experiencing any difficulties through your preferred communication method with us.

Accessible documents

We can produce large print, audio and Braille versions of our documents if required. Using the contact details above, just let us know which version is best for you.

Where are your branches?

Please see our branches page where you can see full addresses and a map to help you find your nearest branch.

What are your opening hours?

You can see a full list of the opening hours for all of our branches here.

How can I find your branch via public transport and where can I park?

Please see our parking and public transport page for the latest information.

Can I arrange to book an appointment?

You can arrange an appointment during the week (Monday to Friday) by calling our Customer Services team, who will arrange for the branch to contact you to book a convenient time.

How can I get help with a general account enquiry?

If you’re registered to access your account online, please login using your User ID and password. Once logged in, you’ll be able to see your balance, transactions and what rate your account is currently earning.

Alternatively, please call our Customer Services team or visit a branch where our teams will be able to help.

How do I make a withdrawal in branch?

You’ll need to provide your passbook when requesting a withdrawal, you may also be asked for additional photo identification.

Branches are able to process a cash withdrawal for branch based accounts only, the daily limit for cash withdrawals is £500 per day per account.

Cheque withdrawals can be processed in branch for up to £99,999.99.

Nominated Accounts - by providing us with details of your nominated account, you can transfer funds by electronic transfer to a linked bank or building society account in a secure manner. Please visit one of our branches with your passbook, proof of the nominated bank account and photo identification, or alternatively you can call our Customer Services team, where we’ll attempt to verify the bank details electronically.

How do I give you feedback about a branch?

We always welcome feedback about our branches, so we can recognise where we did well and where we can improve our service.

To provide your feedback online please go to tellkentreliance.com. To give us feedback over the phone, please call 0800 011 9079 and enter the PIN corresponding to the appropriate branch below:

|

Branch name |

PIN |

|---|---|

|

Chatham |

01 |

|

Canterbury |

02 |

|

Maidstone |

03 |

|

Strood |

04 |

|

Hempstead |

05 |

|

Littlehampton |

06 |

|

Hythe |

07 |

|

Gravesend |

09 |

|

Chichester |

010 |

Opening a Business Savings Account

Including information on whether your company may be eligible for a Business Savings Account, our Opening a Business Savings Account FAQs will help you to get started.

Is my business eligible to open a Business Savings Account online?

To open a Business Savings Account online, your company must be a Private Limited business registered in the UK with fewer than three Directors and major Shareholders.

Your details must also be registered and up to date at Companies House.

Who is an Authorised User?

An Authorised User is an individual who is designated to operate the Business Savings Account on behalf of the Company. At account opening, every Director and major Shareholder of your Company must be set up as an Authorised User so that the necessary identification checks can be conducted on each of them as part of the application.

A maximum of three Authorised Users may operate the accounts of a Company at any one time.

What happens if my Company has more than three Directors or major Shareholders?

Unfortunately if your Company has more than three Directors and major Shareholders, you are not eligible to open a Business Savings Account with Kent Reliance.

What happens if my Company has major Shareholders who are not also Directors?

Unfortunately if your Company has Shareholders who are not Directors, you are not eligible to open a Business Savings Account with Kent Reliance.

Do I need to send in any evidence of identification for my Company or for the Authorised Users to open my account?

Details about your Company and its Authorised Users will be retrieved and verified from Companies House. Once you have submitted your online application, before allowing you to fund the account, we will check the identity and address of each Authorised User. These checks are carried out electronically to make it as easy as possible for you. Sometimes we are unable to carry out the checks electronically and we may ask you to send in some additional evidence of identification by post. We will let you know if we need any additional information at the end of your application.

Details about your Company, Directors and major Shareholders retrieved from Companies House will not be editable within your application.

What happens if the information retrieved from Companies House about my Company is incorrect?

If inaccurate or incomplete information is retrieved from Companies House, before submitting your application, you will need to contact Companies House and correct your details.

How long will Companies House take to correct and update my details?

Companies House should tell you how long it will take to correct and update details held on their systems; however this is usually 2-3 working days.

What is a nominated bank account?

Your Company will need to have a valid UK Bank or Building Society current account held in the Company's name. The account must allow transfers to be made and received electronically and will be known as the nominated bank account. We will need the sort code and account number for the nominated account to complete the application. All deposits into and withdrawals from your Kent Reliance account must be from or to the nominated account.

Will you inform me once my opening deposit has reached my new Kent Reliance business savings account?

Yes, as soon as your opening deposit has reached your Kent Reliance Business Savings Account, an email and SMS (if a mobile number has been registered) will be sent to each Authorised User confirming receipt of funds.

A letter confirming that the new account is open will be sent to the trading address of your Company once the initial deposit has been received.

Taking Money Out

You can withdraw online, by post and in branch, depending on your account terms. Electronic payments from your account can only be credited to your nominated bank account.

How to request a withdrawal/closure

Please note, if you close your last active account, you will no longer be able to access online services. If you send us a secure message to request closure, you will not be able to view a response. We recommend that before closing, you download any information or statements you would like to keep on record.

Online and Postal accounts

You can make a request to withdraw funds or close* your account online (if you have registered for Online Services), by phone or by post.

*To close your account through the online banking service, please use the secure message function to send your closure request.

Branch accounts

If you opened your account in branch, you can make a request to withdraw or close your account by phone, post or by visiting one of our branches.

For notice accounts

Not all notice accounts allow withdrawals without giving the full amount of notice. If your account allows immediate access, it will be subject to a loss of interest.

Please refer to the product specific terms and conditions of your account for further details.

For fixed term accounts

Not all fixed rate bonds allow withdrawals during the fixed rate period. If your bond allows you to make a withdrawal during the fixed rate period, it will be subject to a loss of interest.

Please refer to the product specific terms and conditions of your account for further details.

We understand that things can change unexpectedly and so, if you have an account that doesn’t allow access and you require your savings earlier than your notice period allows or before your maturity date, you can call us to discuss this. We may ask you to help us understand your change in circumstance which may include a request for supporting documentation. Any decision that is made, is at our discretion.

To request a withdrawal or to close your account, you’ll need to provide us with the following:

By post

A signed letter detailing your request or alternatively, you can download and complete a withdrawal/closure form. Please send your request to OneSavings Bank, Sunderland, SR43 4AB.

Online/by phone

- The date you want your savings to leave your account, or when you would like your account to close; and

- The amount you would like to withdraw, and/or confirmation that you would like to close your account (if applicable).

In branch

Please bring your passbook (if applicable) and identification with you. You can find a list of the documents we accept in our Proof of ID and address leaflet.

For details on how to get in touch, visit our contact us page.

Electronic payment requests

Electronic payments (e.g. CHAPS, bank transfers) will only be sent to your nominated bank account. If you change or add a new nominated bank account, please allow additional time for the change to take effect. It’ll take one working day to validate your new nominated bank account, which will result in the payment timescales being delayed by one day. Click here for further information about nominated bank accounts.

If we receive your payment request before 3.30pm on a working day your funds will be transferred to the receiving bank/building society on the same day you requested them.

If we receive your payment request after 3.30pm or on a non-working day (weekends and bank holidays), your funds will be transferred to the receiving bank/building society the next working day.

Please note CHAPS requests cannot be made online. Please call us if you want to make a CHAPS payment, these may incur a charge.

Please be aware that if you send us a withdrawal/closure request by post, you may receive your money a day later than the timescales shown above.

There is no limit on how much you can withdraw, subject to funds being available in the account and your specific terms and conditions.

Cash withdrawal requests

Cash withdrawals can only be made by customers who opened their account(s) in a branch.

Cash (requested at branch during branch opening hours) |

|

|---|---|

| How much can I withdraw? | When will I receive my funds? |

| Our current daily cash limit is £500 | Same day (over the counter) |

| Withdrawals in excess of £500 must be paid by cheque or electronic payment. (e.g. CHAPS, bank transfers) | |

Cheque withdrawal requests

Cheque withdrawals aren’t available for accounts opened online.

Cheques |

||

|---|---|---|

| Method of request | How much can I withdraw? | When will I receive my funds? |

| Branch (requested during branch opening hours) |

Up to £99,999.99 | Same day (over the counter) |

| £100,000 and above | Your cheque will be processed at our Customer Services office and posted to your registered address. Please see tables 4 and 5 of the Savings General terms and conditions for further details. |

|

| Post/telephone |

No limit, subject to funds being available in the account | Your cheque will be posted to your registered address the day your request is treated as received. Please see tables 4 and 5 of the Savings General terms and conditions for further details. |

Running your Business savings account

From how to add deposits to your account, to changing your nominated account, please see our FAQs about running your Business savings account below.

How can I fund my new account?

To deposit into a Kent Reliance Business savings account, you must transfer the funds electronically from your nominated bank account.

You will not be able to fund by CHAPS, cheque or cash.

What will happen if I attempt to deposit funds from an account other than my nominated bank account?

Deposits into your Kent Reliance account that are not from the nominated account will be returned to the account from which they originated without interest.

How do I fund my account by bank transfer?

To make a bank transfer you will need the following details:

Sort code: 62-24-97

Account number: this will be the numerical element of your account reference with a zero added at the front (for example 01234567).

To ensure that your payment reaches your account, please make sure you use your entire account number (with prefix and suffix) as your reference (for example ABC1234567KRB). If you or your bank or building society does not include your reference number when submitting the payment, it may not be possible to match the funds to your account. In this case we may need to then return the funds without interest.

Will you inform me once a deposit has reached my existing Kent Reliance business savings account?

Yes, we will notify the Authorised User once any new deposits have reached your Kent Reliance business savings account.

Is there a limit on how much I can withdraw online?

No, but this is currently under review.

How soon will I receive my money if I withdraw online?

This depends on the day and time you submit your withdrawal request. Full details can be found in our withdrawals page.

How can my business add another Authorised User, Director or major Shareholder to manage the account?

To update Authorised User, Director or major Shareholder information, please download and complete this form and send it to us via secure message.

Can the nominated bank account be changed?

Yes. You must notify us of the change by writing to us with the name, sort code and account number of your new nominated bank account (which must be held in the account holder’s name). You will need to send us an original Bank/Building Society account statement no more than three (3) months old showing the account details. Until such time the update takes effect withdrawals made from your account(s) will still be credited to your existing nominated bank account.

How to make a withdrawal?

Authorised users can withdraw from their account by logging in to your Online Services. Alternatively you can call us or send us a secure message.

To close your account through Online Services, please use the secure message function to send your closure request.

Fraud and Scams

We've built a dedicated fraud hub to help you get the information you need here.

Coming to the end of your deal

As a valued Kent Reliance mortgage customer, we are delighted to offer you access to our Choices mortgage scheme.

The Kent Reliance Mortgage Choices scheme rewards existing customers with a new mortgage deal that requires no valuation or underwriting assessment and is quick and easy to apply for.

Apply for a new mortgage deal online

Find a new Kent Reliance mortgage deal that suits you with our Mortgage Choices Online Portal. Login with your current mortgage deal and we will show you precisely which mortgage deals we can offer you based on your current loan.

If you don't know when your current Kent Reliance mortgage deal is coming to an end, don't worry, we will contact you before your deal expires to notify you of your Choices.

We can only accept original applications via brokers, but if you’re an existing Kent Reliance customer then you can select your new deal yourself online.

We offer products on an eligibility basis alone and do not offer advice, so if you need advice please contact your mortgage broker or find one at unbiased.co.uk.

Contact us by phone

If you are currently on our Standard variable rate, you can contact our Mortgage Servicing Team* for information.

For other mortgage enquiries, you can contact us.

Lines are open: Monday-Friday 9am-5pm, closed on weekends and bank holidays.

*For customer service and training purposes, calls with Kent Reliance may be monitored and/or recorded. We can only provide information about our products and services and we cannot give advice.

Haven't found what you're looking for?

If you're looking for other options such as notifying us that you're moving home or hoping to make an overpayment, then please see our mortgages page.

Bereavement

Supporting you through bereavement

If you’ve lost someone, it may be a struggle to know what steps you need to take next. The information provided is there to assist you through this difficult time. If you need any further support with our bereavement process, please get in touch. If you’d prefer a face-to-face conversation then visit your local branch and our team will be there to help you in the best way possible.

Please note that the information below is intended for savings customers only. If you’re a mortgage customer and you’re looking for additional information, please click here.

With you every step of the way

There can be a lot to think about when you lose someone close to you. That’s why we’ve put together an overview of important things you need to consider during this difficult time.

Step 1

Register the death

It's a legal requirement to do this within five days of the death.

Step 2

Arrange the funeral

Contact a funeral director to begin making arrangements.

Step 3

Is there a will?

Check to see if one exists.

Step 4

Who to contact

Inform any financial or legal bodies as early as possible.

Step 5

Manage the estate

If there is a will, this will help you deal with the estate’s distribution.

Step 6

Seeking further help

Reach out to others if you need emotional support.

Step 1

Registering a death

Every death must be registered at the local registry office. This must be done within five days (eight days in Scotland), unless it has been referred to the coroner.

This is a legal requirement and the registrar provides a formal record of death (a death certificate).

What do I need to be able to register the death?

You’ll need to take the following documents/information with you when registering the death.

Personal information about the deceased (please see the checklist in the ‘Who to contact’ section to assist with this).

Medical certificate – this certificate is free and should be provided by a GP or doctor; or

Coroner’s certificate – in certain circumstances a death has to be investigated by the coroner.

The registrar won’t charge for issuing the death certificate. You may want to think about buying extra official copies of the death certificate, as this can be helpful when dealing with the deceased’s estate.

Step 2

Arranging the funeral

Contact a funeral director to begin making arrangements. Most funerals are arranged and take place within a week or two following death. It’s important to say goodbye. Funerals can be expensive, so it’s worth checking to see if a prepaid funeral plan or life insurance policies exist that may help to cover the cost. If there are sufficient funds in the deceased’s Kent Reliance account(s), these can be used to cover the funeral costs without having to wait for the Grant of Probate to be issued. These funds will be sent directly to the funeral directors.

Step 3

Is there a will?

If there’s a will, it may be held with a solicitor, or at the deceased’s home. A will explains what should happen to the deceased’s estate. It’s their last wishes as to what happens with their assets and funeral arrangements. If there’s a will, it names the executor(s) chosen by the deceased to deal with their estate.

If there isn’t a will

Where the deceased has not left a will, their estate will be dealt with under the laws of intestacy. These laws set out who should deal with and benefit from the estate; this will usually be the next of kin. In some cases, “Letters of Administration”, issued by the Probate Registry will need to be applied for. This document authorises the appointed administrator to deal with the deceased’s estate. We suggest you contact your local Citizens Advice Bureau or solicitor if you require further support with this.

A Grant of Probate or Letters of Administration can also be called a ‘Grant of Representation’.

Throughout this page we’ve assumed that if one is required, the deceased representative will apply for a Grant of Probate. However, there may be cases where Letters of Administration will need to be applied for.

Step 4

Who to contact

When you register the death, the registrar will direct you to the government service ‘Tell Us Once’, which can be found at gov.uk/after-a-death/organisations-you-need-to-contact-and-tell-us-once; this enables you to contact various government departments in one go. This service is offered by most local authorities in England, Wales and Scotland, except Northern Ireland.

If the service isn’t offered by your local authority, then you may need to notify the following:

- HM Revenue and Customs (HMRC)

- The Department for Work and Pensions (DWP)

- HM Passport Office (HMPO)

- Driver and Vehicle Licensing Agency (DVLA)

- Local council

You may also have to inform other organisations. These could be legal, financial and social organisations that need to be informed as soon as possible.

Organisations you may need to contact:

- Banking and Building society providers

- Mortgage provider, landlord or local authority

- Royal Mail (for post redirection)

- Utility companies (water, gas, electric and phone)

- TV licensing and broadband companies

- Any clubs

- Dentists, doctors, hospitals or opticians

- Local church or regular place of worship

- Charities and/or care homes

To make sure that there are as few complications as possible in the notification process, it’s important to gather as much of the following information as you can about the person who has died.

We’ve created a checklist to simplify matters for you: Download checklist

Step 5

Manage the estate

The first step to valuing the estate is to identify the assets and liabilities of the deceased. Liabilities could include personal loans, credit cards, hire purchase agreements, outstanding tax, etc. Assets could include property (less any mortgage), value of personal belongings, shares and monies that are held with other banks or building societies. Any assets will need to be valued in order to distribute the deceased’s estate and if appropriate, to obtain a Grant of Probate.

Grant of Probate